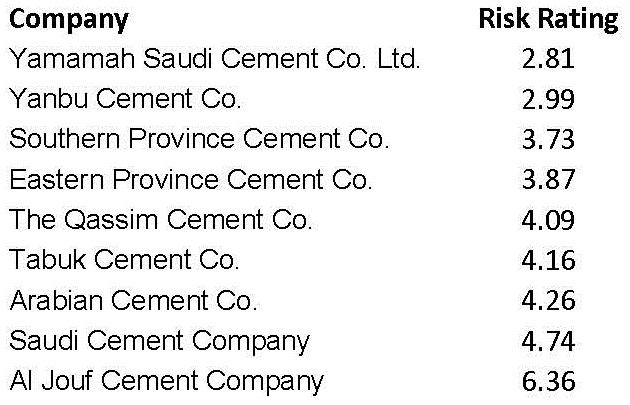

Using 6 Sigma’s Credit Risk System we estimated various Saudi companies’ risk ratings. Of these, the Cement companies showed very low ratings, well below what would be expected in an emerging market. These are displayed as shown below. The question is why?

In an earlier article on Al Marai, a Saudi company involved in dairy products, we posed the question that perhaps the good fortunes of the company are to some extent linked to the amount of subsidy the Saudi Government provides it, in terms of cheap energy, land, water, and food. Now we are asking whether this potential phenomena exits with all Saudi companies, and if so what would be the implications to their risk ratings.

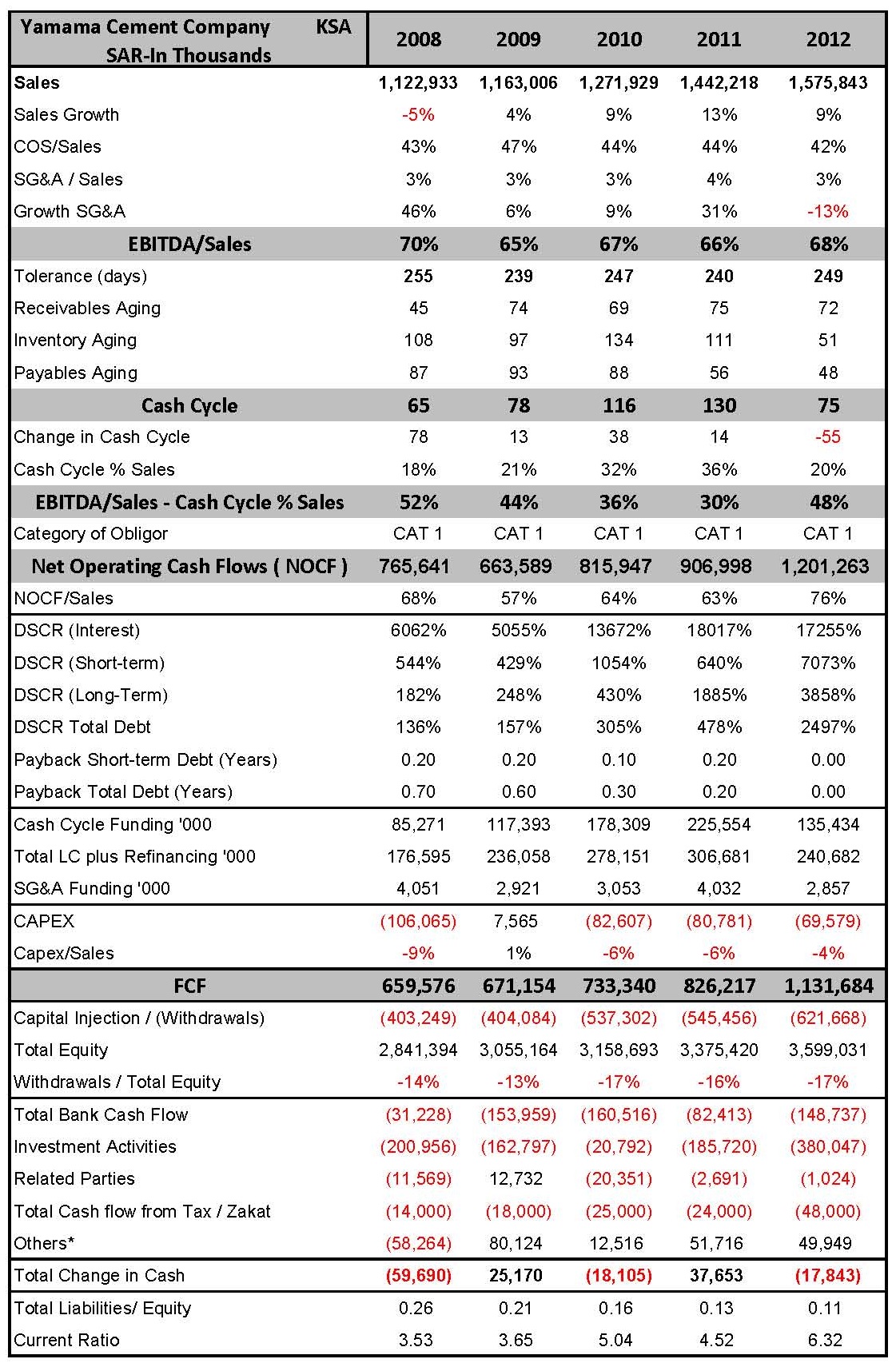

Example Yamamah

Let us look at one example, Yamamah Saudi Cement. Using 6 Sigma’s signature credit risk analysis methodology, this is a “Category 1” company with EBITDA margins in 2012 of 68%, a Cash Cycle of 75 days, and a Net Operating Cash Flows (or NOCF) or 76% of sales (SAR 1.2 Bn). Let me rephrase, for every 1 Saudi Riyal of sales, and there were SAR 1.6 Bn of them in 2012, the company reeled in SAR 1.2Bn in Net Operating Cash Flow, resulting in DSCRs well above 1000%. The only other company that I can think of that can generate as much cash is probably a gold mine, or a government mint office. No wonder its risk rating is a low 2.81.

Example Yamamah

Let us look at one example, Yamamah Saudi Cement. Using 6 Sigma’s signature credit risk analysis methodology, this is a “Category 1” company with EBITDA margins in 2012 of 68%, a Cash Cycle of 75 days, and a Net Operating Cash Flows (or NOCF) or 76% of sales (SAR 1.2 Bn). Let me rephrase, for every 1 Saudi Riyal of sales, and there were SAR 1.6 Bn of them in 2012, the company reeled in SAR 1.2Bn in Net Operating Cash Flow, resulting in DSCRs well above 1000%. The only other company that I can think of that can generate as much cash is probably a gold mine, or a government mint office. No wonder its risk rating is a low 2.81.

Comparative Analysis If we were to compare this cash cow with Lafarge, arguably the largest cement company in the world, we realize that its EBITDA margins in 2012 were lower at 21%, and its NOCF to sales of (coincidentally) an earthly 21%. Its short term DSCR was 115% (above the minimum), and the total DSCR of 29% (at the threshold). Lafarge is risk rated 4.46 on financials. That’s more like it for what is essentially a commodity based company, albeit a manufacturer.

OK so both are category 1 companies, obvious cash cows, but one exceedingly more so than the largest company in the world in this business. What’s its secret?

The answer must again be in government subsidies. Energy is almost free in Saudi Arabia, both for production and transportation. In addition, there were protective laws that limited the issuance of licenses for cement companies in the country, and until recently the importation of cement from abroad. In addition, the government imposed an export ban on cement, which coupled with the recent lifting of the import ban, signals its intention to control supplies and hence prices in the face of an increase in project spending. The latter is estimated at USD 370bn on infrastructure in the short term.

So how much should you finance? As long as Government subsidies (direct or indirect) remain in place, and existing players maintain a strong hold over supply, then cement companies like Yamamah should continue producing the levels of cash they have in the past. In this regard, a banker would be wise to structure the facilities as follows:

1. Aim for 75% of its short term needs of SAR 135 million; and 2. Up to 10 years for its long term needs, for which it has a capacity to borrow up to SAR 8.6 bn. No doubt with the onset of large projects in the kingdom, capacity expansion plans will continue apace.

While the information contained herein is believed to be accurate, neither 6 Sigma nor any of its affiliates or subsidiaries or its employees makes any representation or warranty, express or implied, as to the accuracy or completeness of the information set out in this document or that it will remain unchanged after the date of issue of this document, and accordingly neither 6 Sigma nor any of their respective affiliates or subsidiaries or employees has any responsibility for such information. This document is not intended by 6 Sigma to provide the sole basis of any credit decision or other evaluation and should not be considered as a recommendation by 6 Sigma that any recipient of this document should purchase an equity stake in, provide credit facilities to, or conduct any business with any company(ies) listed in this document. Each recipient should determine its interest in the information provided herein upon such independent investigations as it deems necessary and appropriate for such purpose without reliance upon 6 Sigma.

WANT TO USE THIS ARTICLE IN YOUR NEWSLETTER OR WEB SITE? You can, as long as you include this complete phrase with it: “6 Sigma Group teaches bankers around the world how to become better bankers. Get the “5 Mistakes Bankers Do in Credit Analysis” at www.credit-risk-store.com”