GEMS recently issued a perpetual subordinated Sukuk for USD 200 million, carrying a coupon of 12% (http://goo.gl/G54cz3). This is a company that has a Financial Rating of 3.6 (6 Sigma), a Category 1 obligor in terms of credit risk, and should command very fine pricing. As a comparison, Majid Al Futtaim (MAF), who was rated 4 (BBB) by another party, and who issued a Sukuk for USD 500 million, is paying a coupon of 7.125 % on its perpetual non-callable five year note (currently yielding 7.5%). So why is GEMS paying such high price for its debt? For that matter, why did MAF accept to pay such high price for theirs as well?![]()

From a numbers point of view, GEMS has everything going for it:

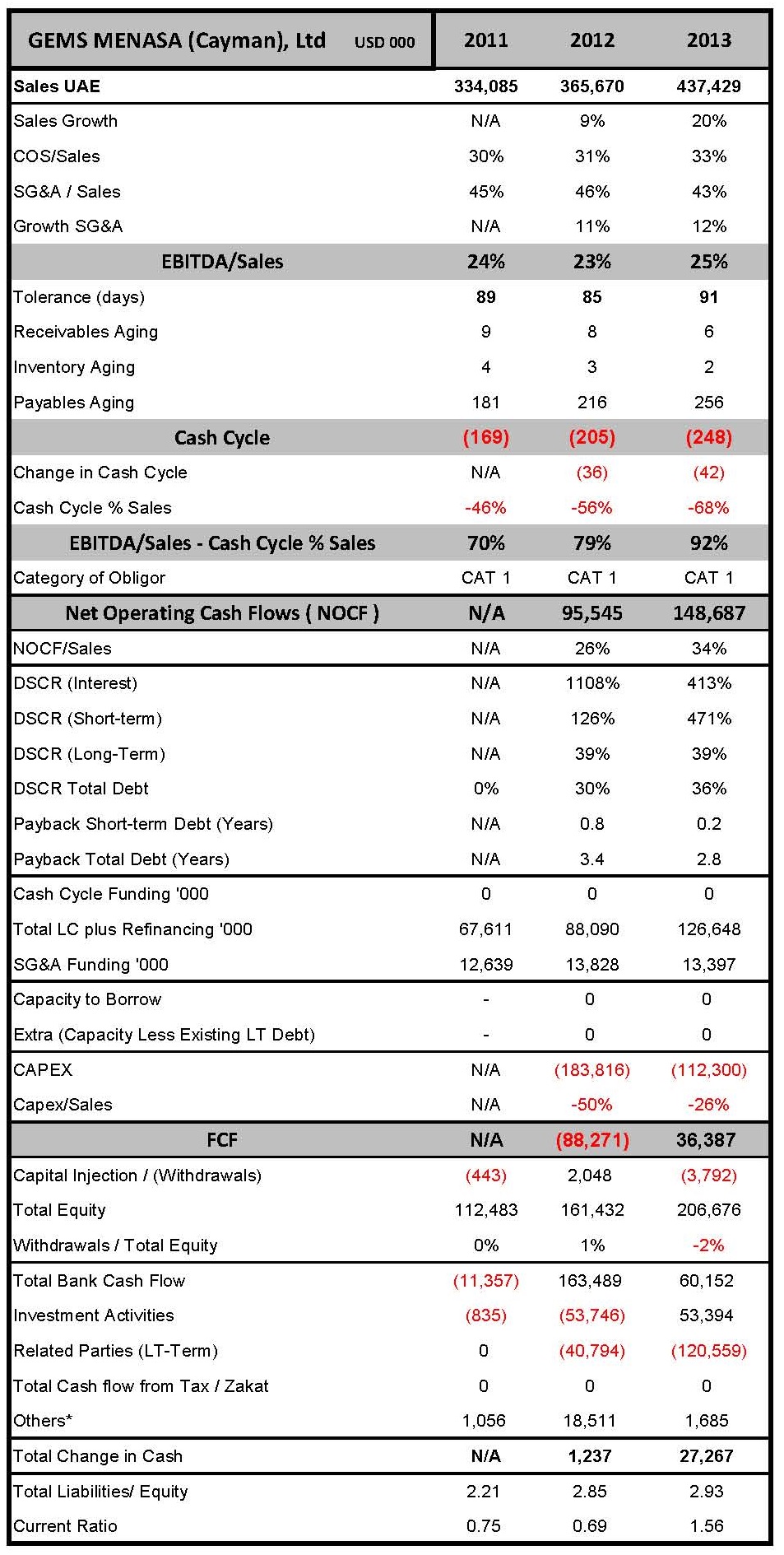

- High Growth rates with a 20% increase in sales in 2013 reaching USD 437 million.

- Sustained Control over expenses. COGS plus SG&A expenses remaining at 76% of sales.

- EBITDA margins were very high, increasing from 23% in 2012 to 25% of sales in 2013.

- Cash Cycle was very negative, reducing from minus 169 days to minus 248 days (minus means receiving cash and taking its sweat time paying suppliers).

- As a result an Engine that increased from 70% of sales in 2011 to a whopping 92% of sales in 2013.

- NOCF was very high relative to sales and climbing, from 26% in 2012 to 34% in 2013, reaching USD 149 million.

From a Credit Risk perspective, these are excellent ratios for any industry. Given the very comfortable DSCRs of 471% on the short term debt and 39% on total debt, the company had a high capacity for borrowing long term of USD 477 million. Subtract the then existing debt in 2013 of USD 385 million, and that leaves an extra debt raising capacity of USD 92 million over as little as a 5 year period. For a 10 year period, it increases to USD 569 million.

Under these circumstances, a risk rating of 3.6 should command pricing of 0.75% to 1% pa maximum. Why on earth are they paying 10.25% above 5 year Libor, and as a vehicle they are going through a very illiquid mechanism, a subordinated perpetual Sukuk?

Is it because:

- The use of the money is for internal purposes, with the funds used to pay off the India subsidiary for the transfer of Indian assets to the UAE company; as well as repay a Private Equity firm to avoid them taking over equity. OK so this is not very kosher and very naughty, but hey they can afford to do so. Besides why did they hook up with a Private Equity firm that wanted to convert Debt to Equity in the first place when the group was doing so well?

- The only other benchmark in this issue is MAF which was rated BBB (that’s the same as GEMS) and they paid 7.125%. Is this the blind leading the blind syndrome? Is the market using MAF and GEMS as experiments? Why go through the perpetual Sukuk way using a Cayman Islands registered company in the first place, and instead simply syndicate the deal amongst regional banks? If paper is the objective, why not issue Commercial Paper, Medium Term Notes or Bonds for longer term? Tapping the Islamic Capital Market in this way was unnecessarily expensive.

- The group already had debts with covenants that restricted higher leverage? Then why not simply reschedule all the debts at once?

- The book-runners, Abu Dhabi Islamic Bank, Credit Suisse and Morgan Stanley were too lax in pricing it or distributing it? Or did they take purposely increase the price to make it easier to sell?

- The banks and investors who were approached tried to squeeze as much as possible out of the deal? Where were the company’s financial advisors to the deal?

- Despite the low rating, the transaction was too risky? Let’s have a look at the risks involved in this business, are they really too large to manage?

Risks Involved in Private Schooling in the GCC:

1. The regional sector has three things going for it:

- Demographics: The GCC population is expected to increase by 30% to over 50 million people in 2020, and its real GDP to grow by 56%. (http://goo.gl/wPaEr)

- Flight to quality which GEMS offers: Private schools, which often teach English-medium curricula, have historically fared better than public schools in TIMSS and PISA tests. (http://goo.gl/4U3zu1)

- Increasing willingness among parents to pay for education: and hence higher potential cash flows.

2. The challenges the schools face are numerous like all other businesses in this region. However these are mitigated to a very large extent as follows:

Growth Risks

- Lack of availability of suitable schools for acquisition to help hasten the growth process. Not a biggy as they can grow organically, as they have done so successfully so far.

- Lack of availability of sufficient funds to grow. Again with so much cash inflow, banks would be short sighted not to support the schools even if investors may shy from venturing.

- Inability to obtain required licenses. This is unlikely given the importance regional governments are placing on education.

- Inability to maintain and implement GEMS standards across all of its school. Governance is an issue and a challenge, which the group has so far managed fairly well.

- The Group may have difficulty locating and hiring quality personnel, and retaining such personnel once hired. This is probably the most pertinent risk all private schools face in the region. There is a flow of eligible international teachers from across the globe (USA all the way to Australia), with varying degree of experience and quality, along with centers of production of quality teachers such as Lebanon. However attracting them into the GCC and having them stay for longer periods will require increased costs in terms of salaries and accommodation. Despite the high cash inflow in this business, increasing revenue over time requires regulatory approval, and sustained excellence in delivering services. In GEMS case, the group has excelled in this in places such as Dubai with its recent acquisition of Excellent scores by the KHDA of 7 out the 9 provided.

Governance and Group Transactions Risks

- The Group does not have depth for its key personnel, Chairman, directors or senior managers. Depth and succession in the organization is an issue that can be managed over time.

- The amounts due from related parties on the balance sheet are principally those from Varkey Group Limited, the ultimate parent company of GEMS, and entities controlled by Varkey Group Limited. The amount due from related parties in FY13 was USD 161.4 million compared to USD 50.3 million in FY12 and USD 1.7 million in FY11. Obviously this practice has to stop and any proper syndication should be able to manage it effectively.

Financial Support / Investor Risk

- The sector is a capital intensive one which acts as a barrier for many investors looking for a quick turnaround (http://goo.gl/1PBICV). OK so what, they can rely on bank debt instead if the debt is managed appropriately.

As you can see from the above, there are no potent reasons why this cash rich group should not be able to acquire favorable financial support. So again, why the weird and convoluted structures? Perhaps the Group has limited financial finesse and was ill-advised. For an educational institution, there is much for them to learn on how to manage their finances. For banks, there is an opportunity to cross sell on the Credit Risk side.

© 2014 6 Sigma Group

While the information contained herein is believed to be accurate, neither 6 Sigma nor any of its affiliates or subsidiaries or its employees makes any representation or warranty, express or implied, as to the accuracy or completeness of the information set out in this document or that it will remain unchanged after the date of issue of this document, and accordingly neither 6 Sigma nor any of their respective affiliates or subsidiaries or employees has any responsibility for such information. This document is not intended by 6 Sigma to provide the sole basis of any credit decision or other evaluation and should not be considered as a recommendation by 6 Sigma that any recipient of this document should purchase an equity stake in, provide credit facilities to, or conduct any business with any company(ies) listed in this document. Each recipient should determine its interest in the information provided herein upon such independent investigations as it deems necessary and appropriate for such purpose without reliance upon 6 Sigma.

WANT TO USE THIS ARTICLE IN YOUR NEWSLETTER OR WEB SITE? You can, as long as you include this complete phrase with it:

“6 Sigma Group teaches bankers around the world how to become better bankers. Get the “5 Mistakes Bankers Do in Credit Analysis” at www.credit-risk-store.com”