Assume you had a bank that operated under Basel’s Standardized approach (which is essentially the majority of banks worldwide today). Also if it were an average commercial bank, its Revenue to Expense ratio would be 2:1. With a Capital Adequacy of 10.5%, and a Return on Capital of 25%, its minimum spread on direct lending would have to be 5.25% to break even.

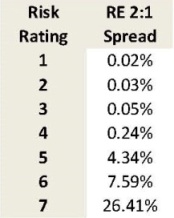

A similar bank operating under IRB would have the following different minimum spreads for direct lines:

From the above, you can gather the following:

-

For obligors that are rated 6 and above, the Standardized bank seems more competitive than a similar IRB bank which is forced to charge more to cover the calculated higher risk.

-

For obligors that are better rated, the IRB bank stands to gain much more economically.

Perhaps this is the reason why many banks opted to shift strategy towards Small and Middle Enterprise (SMEs) markets where spreads are normally higher. The argument goes that the fine pricing for large corporates is uneconomical, and profitability can only be attained dealing with smaller enterprises. This argument is reasonable under the above scenario, except that it is totally flawed in its one dimensional approach.

Why is the argument flawed? In general, entities that are in the SME segment have higher risk ratings. There are exceptions of course, but in general such companies suffer from limited product range, one-man-show operation, lack of depth in management, constricted customer base and so on. Their Engine is usually negative and hence carries a risk rating of above 5 (scale 1-10). However the diversity of ratings amongst SMEs is as varied as that with larger enterprises; and the probability of ending up with rated 7 companies is very high. This should not pose a problem if the bank was rigorous in analyzing its obligor’s credit risks. However banks that operate under the Standardized banner have two major flaws in their operations:

(a) Inability to detect early warning signs as they continue to rely on lagging indicators such as Current Ratio and Leverage; and (b) They use unsophisticated tools and methodologies to assess credit risk and as such lacking in risk rating of obligors.

These two flaws are evident in a surprisingly large number of banks despite the insistence on risk ratings by Central Banks. This is due to the use of substandard risk rating methodologies, general lack of appreciation of credit risk management techniques, and a general misconception of credit risk measurement by Central Banks who are the ultimate judicators.

Consequences: Increased Portfolio Risk Ratings The combination of calculating economic returns using Standardized tools, and lack of rigorous Credit Risk assessments leads banks to capture highly risk rated obligors without realizing it. With a mounting experience of bad debts, the majority end up relying on collateral security as a first way out, inevitably leading to an increased volatility in the quality and economics of the portfolio.

Eroding Competitive edge With the flaws that come with the Standardized approach, banks end up with a reduced ability to take on low risk rated obligors, and experience relatively large defaults in the portfolio. The latter also includes obligors that have very week Engines and/or are unable to generate cash flows. Although there are ways to manage these through Product Programs, such obligors are normally provided with normal working capital financing, resulting in an excessively highly rated portfolio. At a risk rated 7 the minimum spread that needs to be charged is 26.4% as shown in the table above (akin to Credit Cards), which is way above what Standardized banks normally charge.

As if that is not enough, by shifting focus on SMEs where cross sell opportunities are low, the Revenue to Expense ratio of Standardized based banks hardly ever exceeds 2:1. So if a rival IRB based bank were to improve its Revenue to Expense ratio to say 4:1 instead, the minimum spread that it can afford to charge obligors of similarly high ratings (RR 6) improves to 5.06%. This is more competitive than the 5.25% a Standardized based bank would charge for the same risk rated 6 obligor, and hence losses out to competition.

So being a Standardized based bank with a focus on SMEs inevitably erodes the bank’s competitiveness.

So what’s the Solution? Even if you were forced to act under Standardized mode by your central bank (Regulatory Capital):

-

Internally behave as if you were IRB compliant (Economic Capital),

-

Use forward looking methodologies to assess credit risk (cash flow centric),

-

Adopt the RAROC calculator even if from a regulatory point of view you are still in Standardized mode,

-

Stop focusing on the traditional Net Profits and Asset size to judge your performance, and

-

Excel in measuring and improving your Portfolio Risk Rating.

This does not mean that banks should abandon the SME segment. On the contrary there is much to be had in dealing with SMEs both in terms of diversity in the portfolio, and supporting the branch network that is needed to manage the Liability side of the balance sheet. However it is how you deal with SMEs that is important, and this can only be appreciated if the bank were IRB compliant with a strong understanding of managing Probability of Default (PD) and Loss Given Default (LGD). See also our previous article on “How do you manage Credit Risk at your bank?”.

© 2014 6 Sigma Group

While the information contained herein is believed to be accurate, neither 6 Sigma nor any of its affiliates or subsidiaries or its employees makes any representation or warranty, express or implied, as to the accuracy or completeness of the information set out in this document or that it will remain unchanged after the date of issue of this document, and accordingly neither 6 Sigma nor any of their respective affiliates or subsidiaries or employees has any responsibility for such information. This document is not intended by 6 Sigma to provide the sole basis of any credit decision or other evaluation and should not be considered as a recommendation by 6 Sigma that any recipient of this document should purchase an equity stake in, provide credit facilities to, or conduct any business with any company(ies) listed in this document. Each recipient should determine its interest in the information provided herein upon such independent investigations as it deems necessary and appropriate for such purpose without reliance upon 6 Sigma.

WANT TO USE THIS ARTICLE IN YOUR NEWSLETTER OR WEB SITE? You can, as long as you include this complete phrase with it:

“6 Sigma Group teaches bankers around the world how to become better bankers. Get the “5 Mistakes Bankers Do in Credit Analysis” at www.credit-risk-store.com”