Why is everyone clamoring over to buy a large stake in Bisco Egypt? Is the cake and biscuit maker so successful that it will generate fortunes in future? A Credit Risk and Evaluation perspective.

This seemingly well-known Egyptian company seems to have a remarkable historical performance with a financial rating of 4.1 (using 6 Sigma’s Credit Risk System). An investment grade company par excellence, what we consider at 6 Sigma as bordering on a Category 1 company.

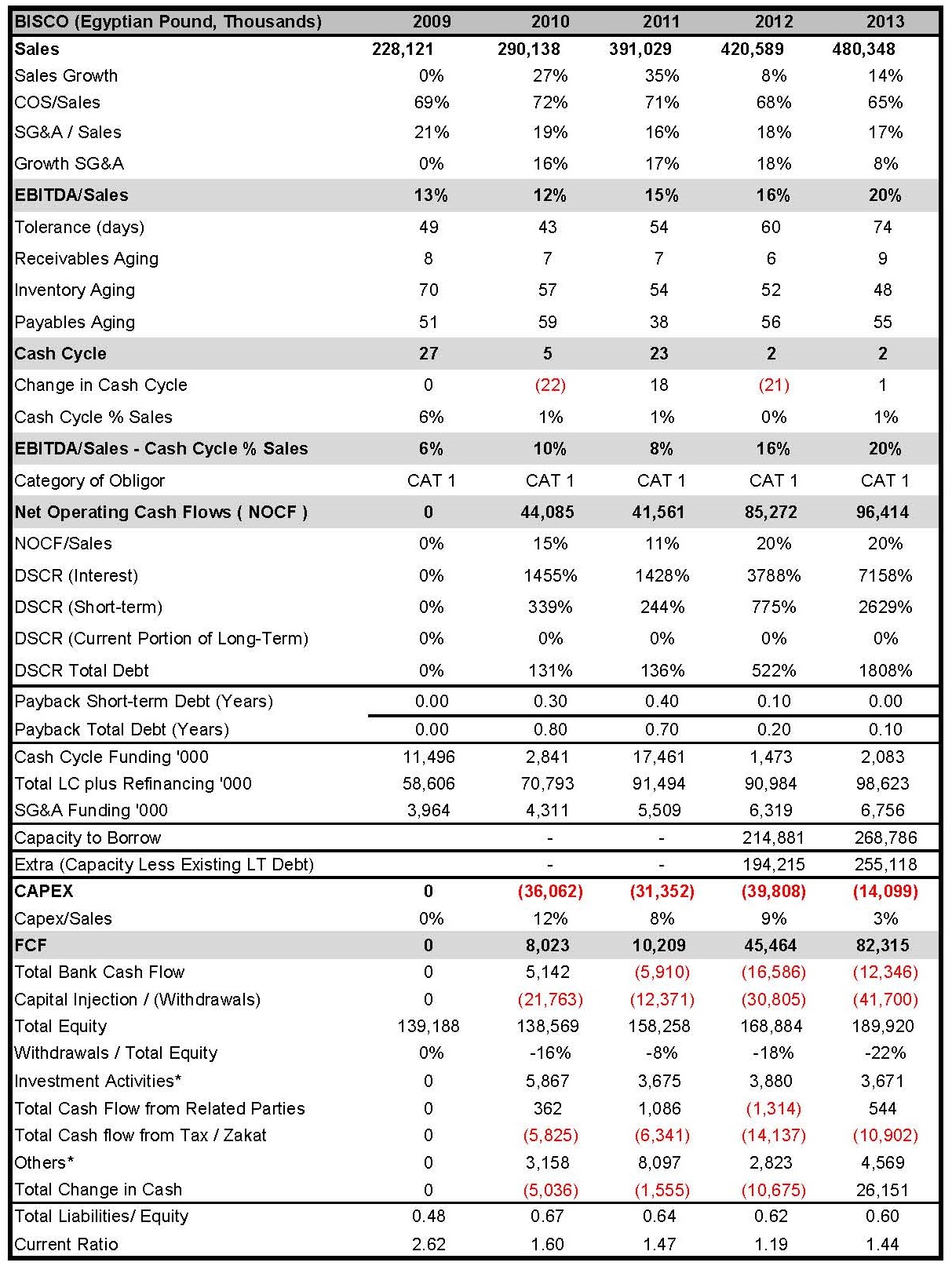

Using 6 Sigma’s signature credit risk analysis methodology, a “Category 1” company is one that continues to generate cash as it grows. As reflected in the company’s 2013 financials, Net Operating Cash Flows (or NOCF) reached a high of EGP 96 million (USD 13.4 million), an impressive 20% of sales (increasing from 15% in 2010 – see table below).

On the very positive side: The reasons for this seem to be in its strong engine, as the following:

- Double digit growth in sales almost every year from 2009 to 2013; reaching EGP 480 million.

- Reducing COGS to Sales from 72% in 2010 to 65% in 2013.

- As a result, an improving EBITDA that increased from 12% to sales in 2010 to 20% in 2013. A remarkable growth that provided the company with ample room to withstand changes in its cash cycle.

- In addition, the company managed to reduce its cash cycle from a high of 27 days in 2009 to just 2 days in 2013 thanks mainly to control over stocks. This represents 1% of sales, which compared with the high EBITDA provided for a Positive Engine of 20%.

- To top it all up, its DSCRs were very healthy, so ample cash flows to meet bank obligations.

- With a high and positive NOCF, and a slight 3% to sales expenditure on Capex, the company managed to produce EGP 82 million in Free Cash Flow (a CAGR of 21% since 2010).

Assuming the above risk rating applies across all the categories of rating, it will then provide for a Cost of Capital of 20%. As its gearing is a low 2.8%, its WACC is 19.6% (as per 6 Sigma Mapping Scale). If its FCF growth rate were a modest 10% pa, the company’s perpetual valuation stands at EGP 1bn (taking into account bank and cash balances at fiscal end 2013). At 15% FCF growth rates, this doubles to EGP 2Bn.

So why are they bidding so low? Perhaps the company needs proper corporate finance advice. In terms of credit risk though, this seems to be a great bankable proposition:

- Without a cash cycle, the company is not in need of short term funding.

- However given its capex requirements (albeit small), it has a capacity to borrow EGP 269 million over a 5 year period. With an existing EGP 14 million of long term debt as at fiscal end 2013, it can easily take on EGP 255 million in addition long term debt. If the period of funding were to be extended to 10 years, this increases to EGP 523 milloon.

If you need help understanding all of this, please contact me on ramzi.watfa@6sigmagrp.com, or simply share your views on the Comments box below.

© 2014 6 Sigma Group

While the information contained herein is believed to be accurate, neither 6 Sigma nor any of its affiliates or subsidiaries or its employees makes any representation or warranty, express or implied, as to the accuracy or completeness of the information set out in this document or that it will remain unchanged after the date of issue of this document, and accordingly neither 6 Sigma nor any of their respective affiliates or subsidiaries or employees has any responsibility for such information. This document is not intended by 6 Sigma to provide the sole basis of any credit decision or other evaluation and should not be considered as a recommendation by 6 Sigma that any recipient of this document should purchase an equity stake in, provide credit facilities to, or conduct any business with any company(ies) listed in this document. Each recipient should determine its interest in the information provided herein upon such independent investigations as it deems necessary and appropriate for such purpose without reliance upon 6 Sigma.

WANT TO USE THIS ARTICLE IN YOUR NEWSLETTER OR WEB SITE? You can, as long as you include this complete phrase with it:

“6 Sigma Group teaches bankers around the world how to become better bankers. Get the “5 Mistakes Bankers Do in Credit Analysis” at www.credit-risk-store.com.